Parametric insurance

To contend with the challenges of climate change and the hardening of the insurance market, companies must develop their capacity to adapt to the risks induced, by implementing practical, prevention measures, as well as exploring the new opportunities offered by parametric insurance solutions.

Parametric insurance differs from traditional insurance

Parametric insurance does not protect against the losses suffered directly by a company, but provides protection via a trigger value for a previously defined index, which opens eligibility for set compensation.

In the current hard market context, parametric insurance can offer a good, albeit partial, alternative. It is possible to remove all or part of a specific risk from an insurance programme, increase its limit or reduce retentions, by taking out a parametric policy.

Bessé has an increasingly important role to play, in collaboration with your teams, to construct the most efficient solutions possible, tailored to suit your needs. The main risk in parametric insurance is the basic risk (difference in value between the loss observed via the index and the loss actually suffered).

Only detailed knowledge of the customer, its market and parametric instruments enables this risk to be minimised.

An innovative additional solution to suit the stakes at hand

Although traditional insurance remains essential, it must be completed by innovative solutions that correspond to the challenges faced by businesses today. Bessé has invested in parametric solutions by creating a specialised team.

THE ABILITY OF INSURANCE CONSULTANTS TO DESIGN THE MOST EFFICIENT SOLUTIONS POSSIBLE IS BECOMING EVER MORE IMPORTANT.

What indexes/parameters can be used?

Climate data, such as rainfall, temperatures, humidity rates, etc.

Measurements related to natural disasters, such as earthquakes, floods, cyclones, tsunamis, etc.

Satellite measurements for forest fires, droughts, plant biomass, for example.

Economic indicators, such as production levels, output rates, number of airport entries, stock market indexes, availability rates, failure rates, etc.

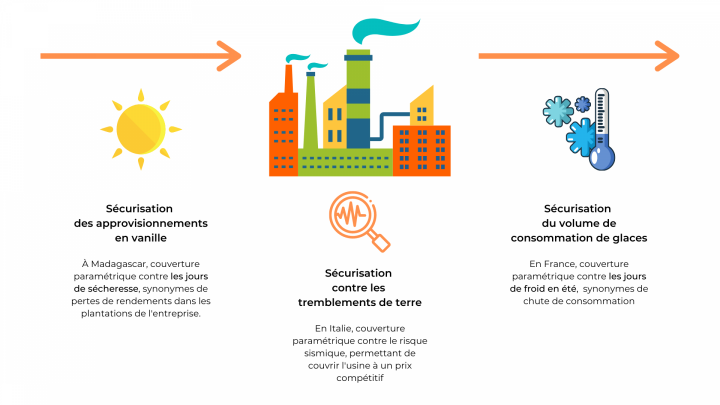

⬅️ Here is an example of parametric insurance applied to an ice cream factory

Parametric Insurance from our customers’ point of view!

For a year now, the Bessé Parametrics team has been assisting all Bessé customers to build “tailor-made” parametric insurance programmes.

Changer vos préférences

There are currently two ways of using this innovative solution:

- It can be used as a defensive measure, providing protection. It also serves to improve or replace certain traditional insurance contracts.

- It can also be used as an offensive measure to cover commercial promises to customers that generate risks.

Read testimonials from Antoine De Zutter, Sales and Marketing Director at Soufflet Agriculture, and Arnaud Grymonprez, Assistant Director of the SCAEL Group, to find out more about the various uses and new opportunities offered by this innovative solution!

The advantages of parametric insurance

EFFICIENT

Big Data and new technologies offer a multitude of data and indexes, which enable extension of the spectrum of insurable risks. Careful study of these data means insurers can propose fairer, more competitive risks costs.

RAPID

As soon as the “trigger” value is observed, the amount of compensation is known, being defined in the policy. There is no need for expertise, and payment can be made within a few hours.

TRANSPARENT

The index comes from a third party data source; it can be consulted by both the insurer and the insured party and cannot be influenced by either. This means a significant reduction in fraud, anti-selection and exclusions, which also bolsters the parties’ faith in the mechanism.

A few key figures

billion in losses caused by natural and human disasters in 2019.

Source : Swiss Ré

Only 25% of annual agricultural losses are insured

of companies have a weather-sensitive activity.